Diplomats negotiate in text. Shipping markets negotiate in fractions of a percentage point. Should the reported memorandum of understanding between the U.S. and Iran be signed this Friday in Switzerland, the political class will watch the ceremony. The people who actually move roughly 20% of the world’s seaborne oil will watch something far less ceremonial: whether war risk premiums start to fall, and how fast.

The two audiences are measuring different things. And right now, the market’s answer is: not yet.

Three possible futures for war risk premiums

The scenario framework matters here because it disciplines the analysis. Strip away the diplomatic language and there are exactly three trajectories for war risk premiums after Friday, each with a different set of winners, losers and routing consequences.

Scenario A: Full de-escalation. The agreement proceeds as currently reported: Iran reopens the Strait of Hormuz to all commercial vessels, the U.S. eases naval restrictions around Iranian oil exports, and oil sanctions receive a specified waiver period. P&I clubs begin a staged reduction in war risk premiums over six to twelve weeks, consistent with how the market normalised after the 2015 JCPOA. Tankers return to Hormuz. Freight rates on Asia–Europe lanes fall as the artificial tightness created by the Cape detour dissolves. The operators who committed to long-term Cape-route arrangements take losses on their hedges. Cargo importers, who have been absorbing elevated costs since late February 2026, emerge as the clear winners.

Scenario B: Partial easing, persistent uncertainty. This is the most plausible outcome. Some P&I clubs return to Gulf underwriting with revised terms. Others maintain restrictions, particularly on vessels with opaque ownership or Russian trading connections, a scrutiny that was already tightening before the crisis. War risk premiums fall from their peak but do not return to pre-2026 levels. The result is a bifurcated routing market: part of the fleet runs through Hormuz and Suez, part stays on the Cape. Operators manage parallel scheduling models at elevated cost. For shipping lines that only just completed the operational adjustment to Cape economics, this is the worst of all possible worlds: premiums still high enough to sting, but not so high as to justify the extra ten days of steaming around Africa.

Scenario C: Deal collapse. The most dangerous scenario is not a failed deal but a failed deal following a temporary one. Markets that price in de-escalation and then face re-escalation react with considerably greater force than markets that never believed the diplomacy in the first place. The actuarial models break down when the political signal is unreliable, and underwriters know it. A deal that collapses within ninety days would likely push war risk premiums above the elevated levels already recorded in March 2026, and would extend the Cape detour through the remainder of the year.

The problem was never just security

Before explaining what a deal might change, it helps to be precise about what the crisis actually produced. The Strait of Hormuz disruption was never only a military event. It was, above all, an insurance event.

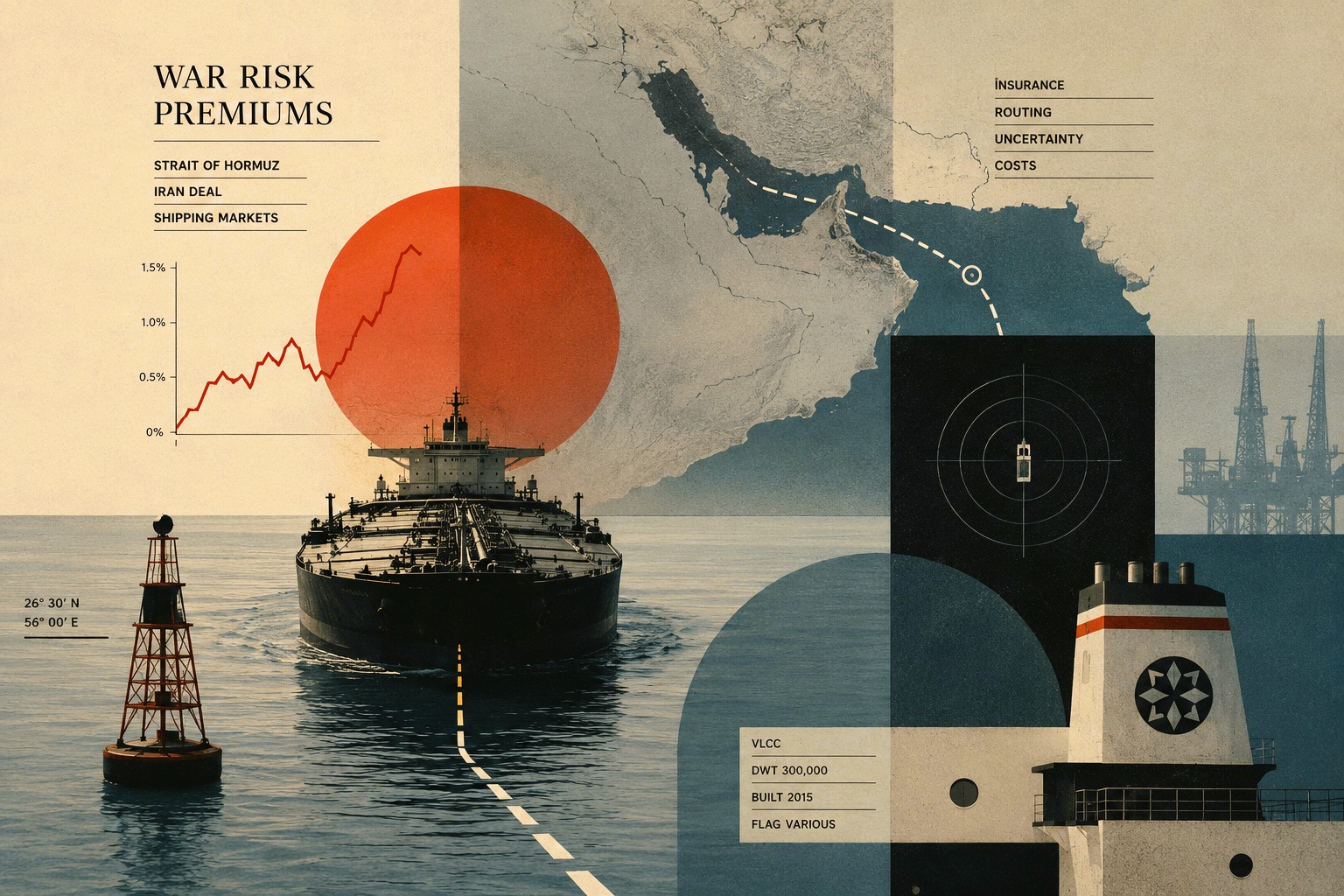

Within 48 hours of the joint U.S.-Israeli airstrikes on Iran on 28 February 2026, the Lloyd’s Joint War Committee redesignated the entire Arabian Gulf as a conflict zone, and all 12 members of the International Group of P&I Clubs — a risk pool covering 90% of the world’s oceangoing tonnage — cancelled certain war coverage with 72-hour notice. Hull war insurance premiums for vessels heading into the Gulf, even without breaching the strait, quadrupled to 1% of ship value for seven days of cover almost immediately. By mid-March, Dylan Mortimer, marine hull war leader at broker Marsh, estimated that average ratings ranged between 0.8% and 1.5% of vessel value. Lloyd’s List reported that Hormuz transits were fetching around 2.5% in most instances and up to 5% for vessels with U.S., UK or Israeli commercial connections, while some underwriters suggested that the highest-risk propositions could attract quotes of 7.5% to 10%.

To put those numbers in context: before the strikes, war risk premiums for Hormuz transits stood at approximately 0.1% to 0.15% of hull value. At 2.5%, a single transit of a $138 million VLCC carries a war risk cost of roughly $3.5 million. Lloyd’s List reported indicative figures of $10 million to $14 million per voyage for the most exposed vessels, to the charterer’s account.

Traffic through the strait fell by close to 95%, according to figures cited by the World Economic Forum, from a pre-war daily average of around 178 vessels. The Lloyd’s Market Association was careful to clarify that coverage remained technically available: 88% of Lloyd’s marine war market participants retained appetite for hull war risks, and over 90% for cargo. The problem, as the LMA stated, was safety concerns rather than outright unavailability. The strait was not uninsurable. It had simply become unaffordable for the overwhelming majority of operators.

What the deal does, and what it does not

Here is what Friday’s agreement will not do: it will not call a single P&I committee into session. It will not restore AIS transparency to shadow fleet tankers that operated for months under false flags, spoofed transponders and ownership structures built to resist scrutiny. It will not reset the actuary’s model.

Insurance markets respond to verified conditions on the ground, sustained over time. The relevant precedent is the 2015 JCPOA: after the nuclear deal was signed, war risk premiums in the Gulf took several months to normalise, and they did so in stages. Underwriters waited for proof that the risk environment had actually changed. They will apply the same logic now, irrespective of ceremony in Switzerland.

By late March 2026, premiums had already eased somewhat — from the 2.5% peak to around 1% — as hopes of an eventual agreement emerged. Yet even at 1%, the Additional War Risk Premium remained up to eight times higher than the pre-war level of 0.1% to 0.15%, according to multiple maritime insurance executives speaking to S&P Global Commodity Insights. That eight-fold gap is the clearest measure of how much distance remains between a diplomatic signal and a functioning market normalisation.

The shadow fleet and the Beijing calculation

One dimension the diplomatic narrative consistently underplays is China. According to Kpler data, China accounted for approximately 90% of Iran’s shipped oil exports in 2025, purchasing an average of around 1.38 million barrels per day. After Iranian exports to Syria halted in late 2024, China became by far Tehran’s dominant crude buyer. That trade was moved almost entirely by a shadow fleet of tankers operating through flag changes, disabled AIS transponders, ship-to-ship transfers and opaque ownership structures.

A sanctioned Iranian oil trade gave Chinese buyers three things: leverage, opacity and discount pricing of up to $7 to $8 per barrel below global benchmarks. A normalised market under a sanctions-relief framework offers greater security of supply but removes all three. Beijing’s strategic interest in cheap, off-books Iranian crude is not identical to its interest in Iran’s geopolitical rehabilitation, and the two can diverge sharply once sanctions relief makes Iranian oil visible to global markets again.

Entities linked to the IRGC are widely reported to benefit from a substantial share of Iran’s sanctioned oil trade, which means normalisation carries domestic political consequences in Tehran as well as strategic ones in Beijing. The shadow fleet does not dissolve with a signature. It migrates. Several hundred tankers, along with the ownership networks and port infrastructure that supported them, will seek alternative irregular trades. War risk premiums in other contested corridors may tighten as displaced tonnage repositions — and the underwriters who tightened AIS monitoring and ownership scrutiny during the Hormuz crisis have not put those tools away. In that sense, the shadow fleet is not a footnote to the war risk premium story. It is one of the reasons war risk premiums will not return to pre-war levels as quickly as the diplomats would like.

The premium that does not simply disappear

The structural conclusion that shipping markets have been drawing since late 2023 is uncomfortable but clear: the era of frictionless transit through critical chokepoints is finished. The Houthi episode in the Red Sea did not end when the bilateral ceasefire was announced in May 2025. Traffic never fully returned to Bab el-Mandeb at pre-2024 volumes, and the Hormuz crisis layered a second major disruption on top of a first that had never properly resolved. As GeoTrends documented in April, the rerouting around the Cape of Good Hope had already begun reshaping African port infrastructure in structural rather than temporary ways.

War risk premiums are not purely a function of the news cycle. They are a function of demonstrated precedent. The precedent now established is that both major Gulf chokepoints can be disrupted simultaneously, that the insurance market responds by withdrawing or drastically repricing cover within 48 hours, and that tanker traffic can fall by close to 95% within a week. No memorandum of understanding erases that precedent from an actuary’s risk model.

What Friday’s deal can do is begin the process of rebuilding the risk premium downward. It supplies the starting condition. The rest depends on verified implementation over months, not on the quality of the ceremony — and on whether the political architecture holds long enough for underwriters to reclassify the Arabian Gulf from active conflict zone to manageable risk corridor.

The shipping market will be watching, as it always does, in fractions of a percentage point.