Freight markets are beginning to price Middle East conflict risk back into global trade flows. The Strait of Hormuz, the Red Sea and the Suez Canal form a single operational corridor for energy and container traffic between Asia and Europe, and even without a formal closure, risk perception alone is shifting routing decisions. Selective diversions, longer voyages and higher bunker consumption are already tightening effective capacity. In shipping, distance is cost — and cost moves quickly.

This is not yet a supply shock; it is a risk repricing phase. War-risk premiums are rising, tanker sentiment is firming, and container capacity is being rebalanced as operators hedge exposure. Markets do not wait for blockades. They react to probability. What is unfolding is a familiar dynamic: uncertainty enters first, freight follows, and energy prices transmit the pressure across the system.

Shipping and energy enter a new phase of risk

The rising tensions in the Middle East are bringing back a familiar but highly important source of instability for the global economy: the security of major sea trade routes. Military operations involving Israel and the United States against Iran, along with increased military presence in the Persian Gulf, have already triggered precautionary reactions from governments, insurance companies, and shipping groups, even before any real disruption to navigation has occurred.

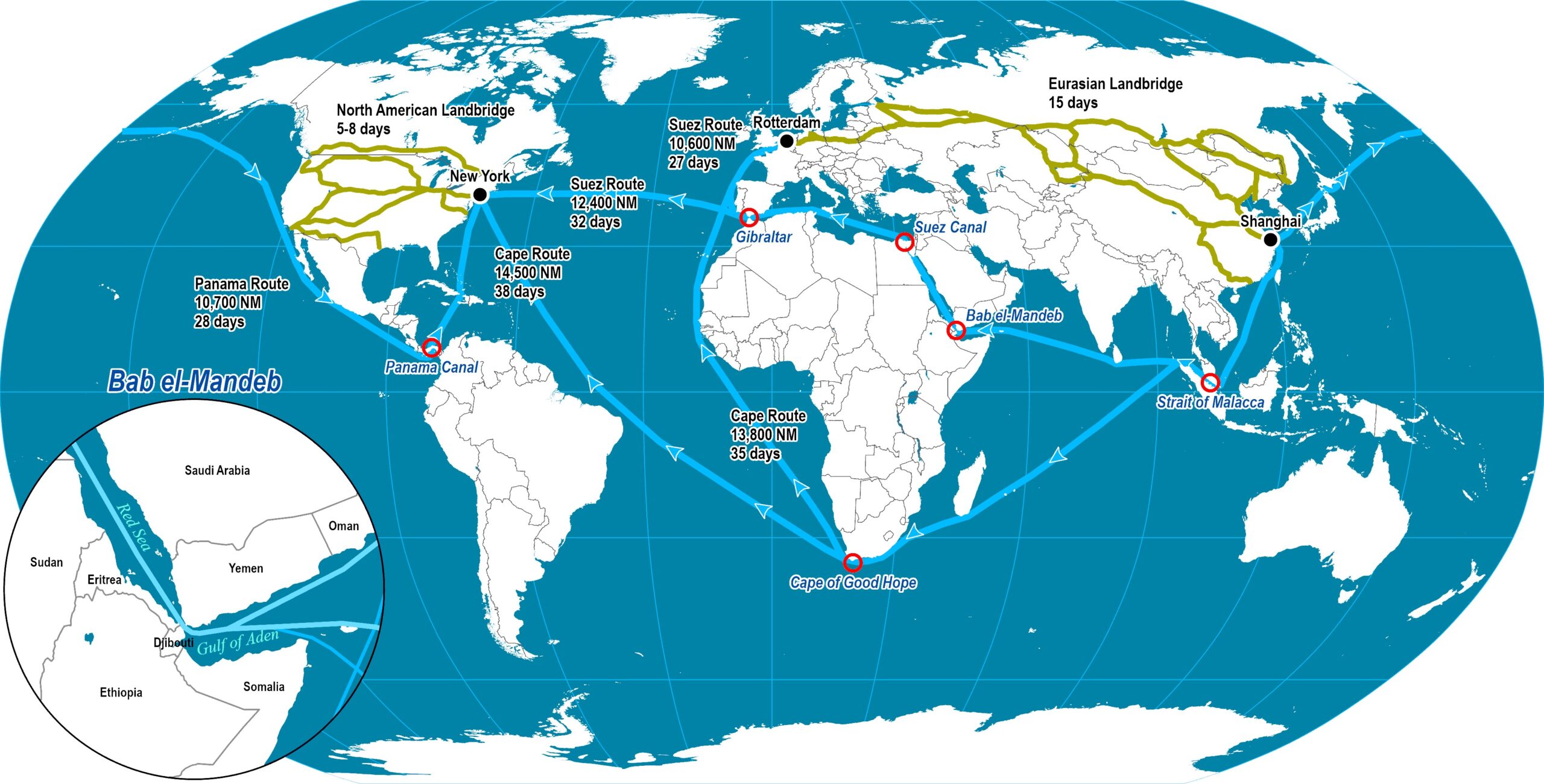

Market attention is mainly focused on the Strait of Hormuz, the Red Sea, and the Suez Canal—three locations that function as a single system for the flow of energy and goods between Asia and Europe. Any disruption in one of these areas immediately affects the entire supply chain.

Some large container shipping companies have already started selective route changes, choosing to sail around the Cape of Good Hope instead of passing through the Red Sea and the Suez Canal. This decision is not due to closed sea lanes, but to a higher perception of risk.

The Suez Canal and the capacity effect

The importance of the Suez Canal remains critical for Asia–Europe trade, as it provides the shortest connection between the two markets. When ships avoid the area, voyages become about ten days longer, increasing fuel consumption and reducing available shipping capacity. In practice, fewer ships are available at the same time, which creates upward pressure on freight rates, even without higher demand.

The main concern remains the Strait of Hormuz. A significant share of global oil exports passes through this narrow passage, making it vital for the energy security of both Asia and Europe. Almost 3,000 ships cross the area every month, carrying energy cargoes and goods. This means that even limited incidents can influence energy markets and push tanker freight rates higher.

Energy exposure and escalating costs

The economies most exposed are mainly large Asian industrial countries that depend heavily on oil imports from the Persian Gulf. Europe is affected mostly through supply chains and higher transport costs, while, for Egypt, fewer ship transits through the Suez Canal directly translate into lost revenue.

Rising oil prices are the main channel through which geopolitical tension affects shipping. Fuel remains the largest operating cost for ships, and any increase gradually passes into freight rates. At the same time, war-risk insurance premiums rise when an area is classified as high risk, adding further operational costs.

Iran has the capability to disrupt or temporarily interfere with navigation, but a prolonged closure would trigger strong international reaction and serious economic consequences for all parties involved. The most likely scenario is a period of increased uncertainty, where risk remains high without a complete interruption of traffic.

At the same time, the possibility of renewed attacks in the Red Sea keeps the market on alert. Experience from recent months has shown that shipping reacts quickly when security is questioned, even if incidents are limited. Avoidance of an area by major shipping lines is enough to affect global routes and delivery times.

The overall picture suggests that shipping is entering another phase of geopolitical risk, where uncertainty itself becomes a major cost factor. Even without an official blockade of sea routes, increased threat levels are enough to change routes, influence freight rates, and ultimately raise the total cost of global trade.