The shipping market faces a mixed outlook in Q4 2024 through to 2027, driven by geopolitical tensions, economic uncertainty, and shifting trade dynamics. Different vessel segments—tankers, bulkers, containers, and gas carriers—are each subject to distinct market forces that present both risks and opportunities for shipowners, operators, and investors. Based on the latest data from VesselsValue (source: blog.vesselsvalue.com), this forecast provides a comprehensive look at the key trends shaping the shipping industry over the next few years. Below, we outline the expected market developments for each vessel category.

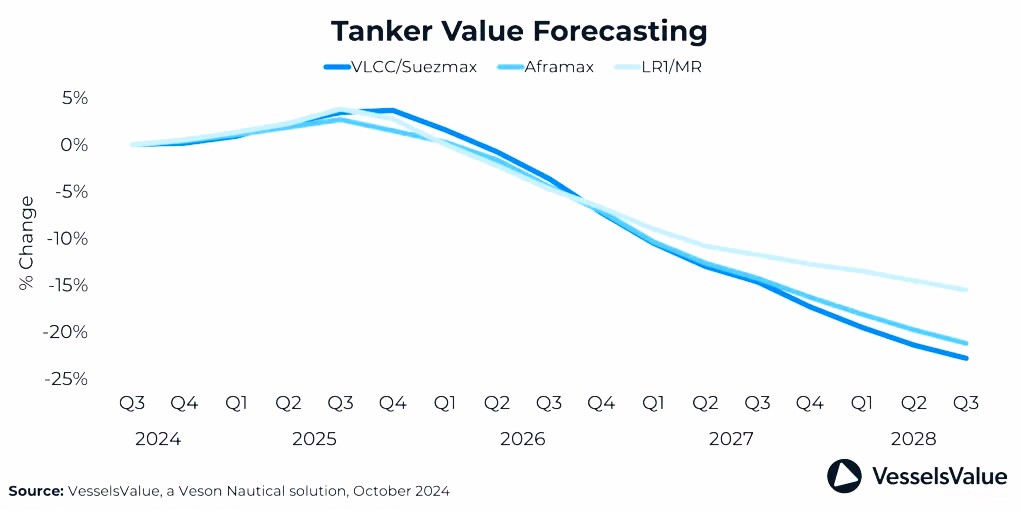

1. Tankers

Key drivers

- Volatility in crude oil prices, shifts in Russian oil exports, and geopolitical tensions (especially in the Red Sea) will continue to shape the tanker market.

- Ongoing preemptive measures in key shipping lanes such as the Suez Canal and the Bab Al Mandeb Strait could lead to longer routes, increasing ton-mile demand.

- Chinese demand for oil, driven by refinery runs and high crude imports, remains a critical factor for market stability.

Market outlook

- The global tanker orderbook in 2024 remains robust, matching 2023 levels at 36 million DWT—a level not seen since 2017. However, deliveries for 2024 are expected to be low, with a significant increase in deliveries from 2025 onwards.

- The orderbook-to-fleet ratio is currently at 12% and is projected to grow, signaling optimism about future demand.

- Tanker rates are expected to remain strong due to continued ton-mile growth, particularly as Russia’s oil exports to Europe decline and shipments shift to more distant suppliers in the Middle East, Latin America, and the US.

- A potential risk to the tanker market is the ongoing conflict in the Red Sea. Should these tensions subside, a return to the Suez Canal could lead to a correction in the market, impacting ton-mile demand.

Conclusion for tankers

The tanker market will experience strong demand in the short term, with increasing orders supporting fleet growth. However, the market faces uncertainty due to geopolitical tensions and fluctuating oil prices.

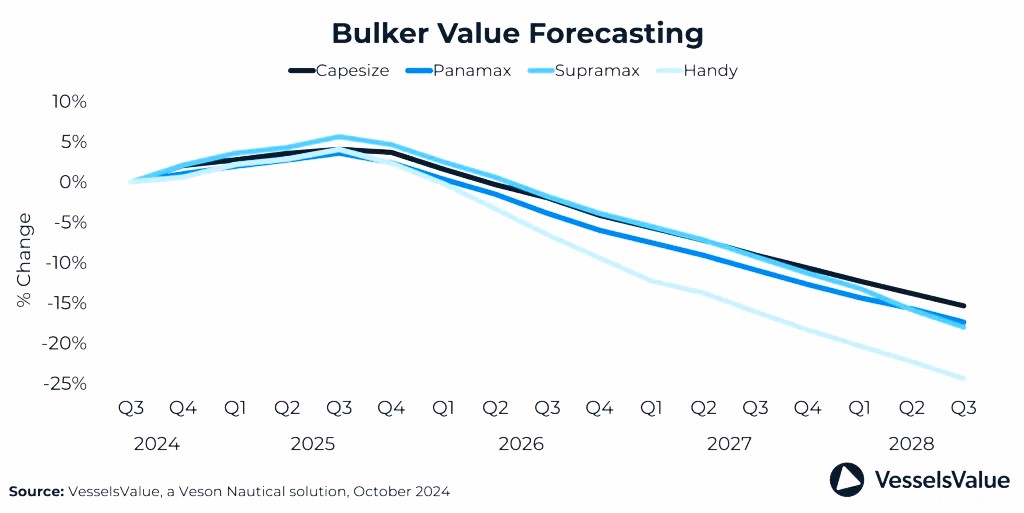

2. Bulkers

Key drivers

- A low orderbook and limited supply growth suggest a fundamentally strong Bulker market, despite moderate demand expectations.

- Shifting trade flows, particularly in iron ore, and the ongoing war in Ukraine have extended shipping distances, pushing up ton-mile demand.

- China’s slowing real estate market is dampening steel production, which in turn could affect overall demand for dry bulk shipping.

Market outlook

- Bulker values have increased significantly over the past year due to improved sentiment in the market. However, given that freight rates have already risen, potential upside is somewhat limited.

- Rerouting, such as taking longer routes around the Panama Canal and Suez Canal, has driven up ton-mile demand this year. This trend is expected to continue, especially with ongoing uncertainties in the Red Sea.

- The China-Brazil iron ore trade is a major driver for bulkers, with Vale expanding capacity, and the opening of the Simandou iron ore mine in Guinea in 2025 will further fuel ton-mile demand.

- Panama Canal congestion is expected to improve by Q4, but this will not fully mitigate the impact of ongoing geopolitical events, especially the war in Ukraine.

Conclusion for bulkers

The bulker market is likely to experience modest growth, with strong demand due to increased ton-mile values. However, there are potential risks from supply chain disruptions and weaker demand for steel from China.

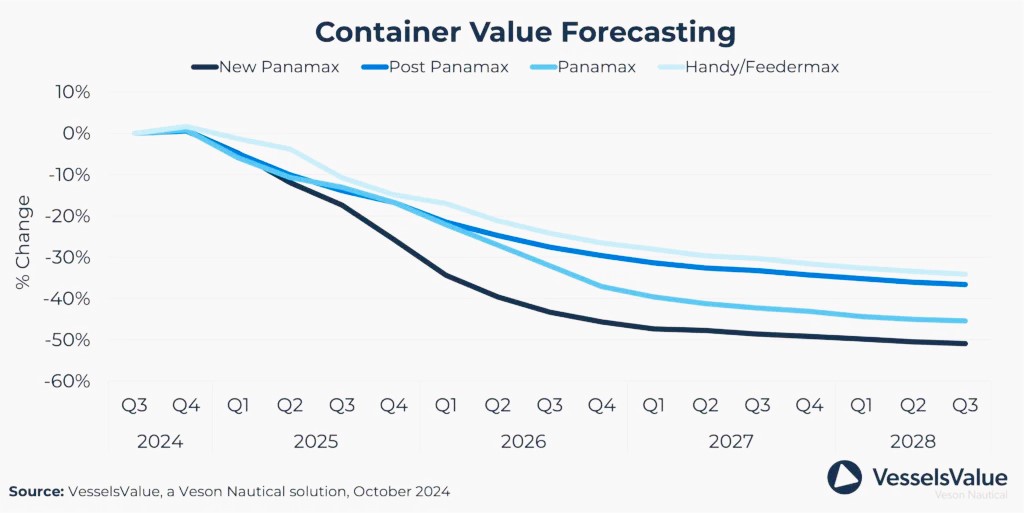

3. Containers

Key drivers

- The demand for container shipping is positive in 2024, with significant growth in the Transpacific eastbound trade (up 22.4%). However, the overall market faces challenges from a growing supply of vessels and anticipated declining rates from 2025 onwards.

- The Red Sea conflict has had a significant impact on shipping routes, leading to longer sailing distances and port congestion, which has driven up freight rates in the short term.

Market outlook

- Container shipping has benefited from high freight rates, which are expected to remain elevated in the short term. However, as new vessels enter the market—almost 8 million TEUs are expected to be delivered over the next few years—there will be an oversupply, putting downward pressure on rates.

- The orderbook for new containers has surged, with 2 million TEUs ordered in Q4 2024 alone, indicating a record-high demand for new vessels.

- Despite high freight rates, scrapping activity in the container sector has been muted. However, older non-eco vessels may face higher operational costs due to tightening CO2 emissions regulations (EU ETS), leading to more vessels being sent to the scrapyard in the coming years.

- The market is expected to face a supply surplus once the ongoing rerouting trend around the Red Sea slows.

Conclusion for containers

The container market faces both strong demand in the short term and increased competition in the long term as new vessels are delivered. The expected supply surplus could put downward pressure on rates from 2025 onwards.

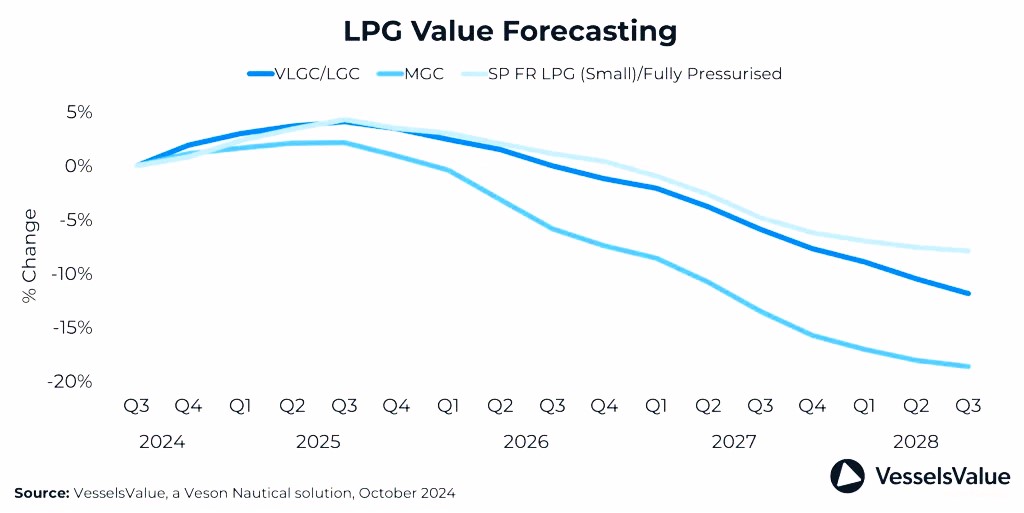

4. Gas carriers (LNG/LPG)

Key drivers

- US LPG production is expected to grow at a more moderate pace in 2024, with a forecasted growth of 4.4%. Despite strong first-quarter export activity, the hurricane season may disrupt production and exports in the latter part of the year.

- Demand for LPG in Asia is set to rise, especially with increased use in PDH plants (Propane Dehydrogenation) and growing domestic consumption, particularly in China.

Market outlook

- The orderbook for VLGCs (Very Large Gas Carriers) is strong, with over 51 vessels ordered, expected to be delivered between 2026 and 2027. However, these vessels are unlikely to be used for ammonia transport in the short term and will instead continue to carry LPG.

- The Panama Canal is a critical factor for LNG/LPG transits, with expected improvements by 2025 that will reduce seasonal disruptions. However, recent droughts and the expected increase in traffic could lead to continued capacity constraints in the short term.

- The global shift towards green ammonia is expected to pick up pace by the end of the decade, although current ammonia volumes remain insufficient to support widespread trading.

Conclusion for gas carriers

The gas carrier market will face moderate growth, with strong demand for LPG exports, particularly from the U.S. However, logistical challenges such as Panama Canal congestion and limited ammonia volumes may limit overall growth.

Shipping market outlook (Q4 2024 to 2027)

The outlook for the shipping industry through 2027 presents both risks and opportunities across different vessel types. The tanker market is poised for growth, driven by ton-mile demand, while the bulker market shows a strong, but moderately constrained, outlook due to geopolitical risks and limited steel production. The container sector faces short-term benefits from high freight rates, but an influx of new vessels could result in a supply surplus by 2025, pushing rates lower. Lastly, the gas carrier market is stabilizing, with continued demand for LPG but facing logistical challenges in key trade routes.

The overall shipping industry is influenced by shifting trade flows, economic uncertainties, and geopolitical developments, making it a dynamic market requiring close attention from stakeholders.