Yesterday, Iranian Foreign Minister Abbas Araghchi declared the Strait of Hormuz “completely open” for commercial vessels for the duration of the ceasefire, on a coordinated route. Stocks surged. Oil prices dropped. President Trump thanked Tehran — then confirmed, in the same sentence, that the U.S. blockade of Iranian ports would remain “in full force” until a permanent peace deal was concluded. The markets processed the headline. The shipping industry processed the fine print.

The fine print, as ever, is where the story lives.

Forty-seven days that changed the calculus

Since February 28, when the United States and Israel launched Operation Epic Fury and Iran responded by effectively sealing the Strait of Hormuz, the global energy system has been running on reserves, rerouted tonnage, and wishful thinking. The numbers are not abstract: roughly 20% of the world’s seaborne oil trade and 20% of global LNG transit this 34-kilometre corridor. So does 30% of internationally traded fertilizer — a fact that receives considerably less media attention until crops begin to fail.

The Islamic Revolutionary Guard Corps (IRGC) confirmed the closure on March 2 and subsequently carried out 21 confirmed attacks on merchant vessels. War-risk insurance, the invisible scaffolding of global maritime trade, effectively collapsed. Nearly 20,000 mariners found themselves stranded in the Persian Gulf. And the world quietly learned that “chokepoint” is not a metaphor. It is a precise engineering term.

The mines nobody can find

Here is the operational problem that no diplomatic announcement can dissolve: Iran does not know exactly where all its mines are. According to reporting by The New York Times, the mine-laying operation was, to put it charitably, disorganised. Documentation was incomplete, and ocean currents have since done what ocean currents do.

Paul Heslop of the UN Mine Action Service explains why this matters more than most commentary has acknowledged. Sea mines operate across four dimensions: three spatial and one temporal. An area cleared at dawn can be contaminated again by midnight, as tidal surges redistribute ordnance with complete indifference to ceasefire schedules. Any convoy transiting the Strait of Hormuz, even under the most favourable conditions, must move through a swept corridor just a few kilometres wide — preceded by minesweepers, governed by a dynamic clearance that must be repeated continuously.

That is not an open waterway. That is a controlled funnel, entirely contingent on the goodwill of a state that cannot fully account for what it deployed. The U.S. Navy began clearing operations on April 11. The IRGC promptly claimed that an American vessel turned back under warning the same day. One hopes the Iranians retain at least a general sense of where those particular mines are.

Insurance: the barrier that outlasts the ceasefire

Before February 28, war-risk insurance premiums for a single transit through the Strait of Hormuz ranged between 0.15% and 0.25% of a vessel’s hull value — roughly $150,000 to $250,000 for a Very Large Crude Carrier valued at $100 million. By the peak of the crisis, underwriters were quoting 5% to 10% per transit. At 5%, that same $100 million tanker faced a single-transit insurance bill of $5 million. For larger vessels — those valued between $200 million and $300 million — premiums exceeded $7.5 million to $15 million in the most elevated scenarios.

The Lloyd’s Market Association’s Joint War Committee expanded its high-risk designation to cover the entire Persian Gulf, triggering mandatory additional premiums and prompting P&I clubs to revise or terminate standard war-risk extensions. Ports, charterers and lenders routinely refuse uninsured or underinsured vessels, so the institutional response amplified the commercial impact well beyond the insurance market itself. In response, the Trump administration directed the U.S. Development Finance Corporation to establish a reinsurance facility of up to $40 billion. When a government must underwrite a commercial shipping route with $40 billion in public money, it is worth noting that the private market has already reached its verdict.

As the World Economic Forum observed, insurance functions as the invisible infrastructure of global trade — precisely until risks become too concentrated and too unpredictable to model. That threshold was crossed weeks ago. A ceasefire announcement does not reset it.

“This moment requires clarity. So let’s be clear: the Strait of Hormuz is not open. Access is being restricted, conditioned and controlled. That is not freedom of navigation. That is coercion.”

— Sultan Ahmed Al Jaber, CEO, ADNOC

400 want out. 100 are willing in. Do the maths

Even if every mine were swept, every premium normalised, and every ceasefire commitment honoured, a structural asymmetry in the Strait of Hormuz would still take months to resolve. Roughly 400 loaded oil tankers are waiting inside the Gulf to exit. Approximately 100 empty tankers are willing to enter.

The commercial logic is straightforward: no owner voluntarily sends an empty vessel into a theatre from which it might not emerge for weeks. “A two-week ceasefire and a ceasefire that’s fragile — I don’t think that would give the confidence (to ship operators) that is needed,” said Lale Akoner, global market analyst at eToro. Matt Smith of Kpler is more precise: even if the strait reopened today, oil flows would likely not return to pre-war levels until July.

The container picture is equally stark. Peter Tirschwell, Vice President for Maritime and Trade at S&P Global Market Intelligence, notes that roughly 100 container ships wait to leave the Gulf while virtually none wait to enter. The 30% of global fertilizer production normally routed through this corridor remains bottled up — not primarily because of politics, but because the inbound vessels to collect the next wave of cargo simply do not exist in sufficient numbers. “The capacity,” Tirschwell observed, “does not exist to easily reroute those cargoes.” The market’s first relief rally, in other words, may be obscuring a far more stubborn logistical shortage.

The carriers have already told you what they think

Maersk has now issued 22 consecutive operational updates on the Middle East situation. Its most recent language is instructive in its careful precision: “While the ceasefire may allow some transit, full maritime certainty is not yet assured.” The company adds that it is “proceeding cautiously” and that visibility “remains low.” This is not the language of a carrier preparing to resume normal service. It is the language of a carrier waiting for conditions it does not yet see.

Rolf Habben Jansen, CEO of Hapag-Lloyd, was somewhat more direct on a customer call, confirming that even under ceasefire conditions, a minimum of six to eight weeks would be required before a fully normal network was operational. The conflict is currently costing Hapag-Lloyd roughly $55 million per week in additional operational costs — a figure the company acknowledges will reach freight markets. One shipping executive, speaking anonymously to CNBC, offered the clearest formulation of commercial reality available: “If we were deciding to transit, we need absolute guarantees about the safety of our crew members.”

When the two largest container carriers on earth frame the situation in these terms, the appropriate analytical response is to take them at their word.

What kind of waterway emerges from this

The central question is not whether ships resume transit this week or next. It is what kind of waterway emerges from this crisis. Iran’s supreme leader Mojtaba Khamenei stated explicitly that Tehran “will bring the management of the Strait of Hormuz into a new stage” during negotiations with Washington. Iranian lawmakers have already moved to codify sovereign authority over the strait, and a toll-collection regime confirmed by Gulf Cooperation Council officials is already operational — in clear violation of international maritime law. IMO Secretary-General Arsenio Dominguez left no room for ambiguity: “Countries do not have the right to introduce payments or charges on these straits.”

The ceasefire is the interval between rounds. The real negotiation is over who controls the corridor permanently — and on what terms.

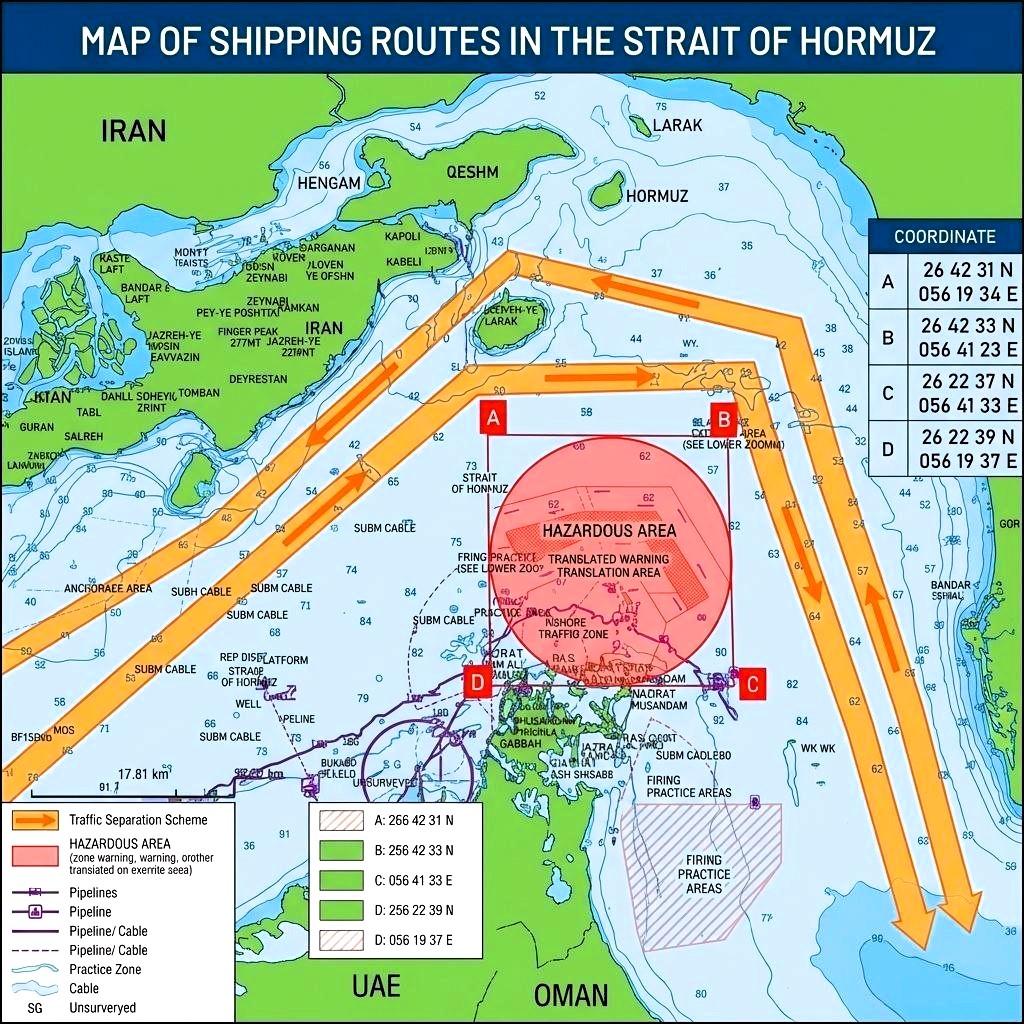

That question moved from abstract to operational today. Ebrahim Azizi, chairman of Iran’s parliamentary National Security Committee, posted a map of IRGC-designated transit routes and stated that the time has come to “comply with the new Maritime Regime of the Strait of Hormuz.” The message was unambiguous: only vessels holding IRGC Navy clearance may use the designated corridors. “These regulations,” Azizi wrote, “are set by Iran, not by social media posts.” The IRGC had already published this map in early April, directing ships away from the traditional Omani-coast route and toward a more northerly corridor closer to Iranian territory — ostensibly to avoid mines, but structurally consolidating Iranian control over the chokepoint’s geometry. A Lloyd’s List spokesperson assessed the situation plainly: “We know Iran is essentially still in control of the Strait, and the assumption is that ship owners will still need to seek permission from the IRGC — and how that’s going to work is still not clear.”

For the shipping industry, these consequences will outlast any two-week truce. War-risk premiums for the Persian Gulf will not return to pre-crisis levels for years. Fleet repositioning toward the Atlantic Basin now reflects durable risk logic. And the precedent of a $40 billion state-backed reinsurance facility keeping a trade artery commercially viable has now been set, with implications that extend well beyond this conflict. Hamid Hosseini, spokesperson for Iran’s Oil, Gas and Petrochemical Products Exporters’ Union, offered a remark that deserves to be read slowly: “Iran is not in a rush.”

Neither, it appears, are the ships.